P3 Reduction in Meralco’s Rate An Achievable Dream!

87% or P2.60 will not even come from Meralco’s pockets but from various pass-on charges on which Meralco had been claiming for many years they don’t make money and only act as collectors. Generation charge, transmission charge, systems loss, VAT, universal charges. Only 13% or P0.40 per kwh will come from Meralco’s excess distribution charges due to the questionable “performance based ratemaking” or PBR.

Meralco therefore should have no problem cooperating in keeping with its commitment to public service and true corporate social responsibility.

MSK’s Power Cost Reduction Solution

On October 8, 2014 the Matuwid na Singil sa Kuryente Consumer Alliance (MSK) shared with the Department of Energy’s Multi-Sectoral Task Force to Find Ways to Reduce Electricity Prices our recommendations on how to reduce Meralco’s power rate by Php 3.00 per kwh.

We cited the specific bases for the 10 areas for reductions and why we believe there is room for eliminating excesses that result to high rates. The Philippine Independent Power Producers Association (PIPPA) for its part analyzed that the Philippines need a reduction of P2.00 per kwh will make us power competitive with our Asian neighbors.

Meralco, with their well-oiled image management machinery, dismissed the suggestions to have “no basis”. They even went on TV saying the same thing.

MSK is starting a series on the 10 recommendations with further details to help everyone appreciate that this is a realistic target and not a wild number by a consumer group. The Ibaba ng P3 Movement is not an impossible dream.

But What is Meralco’s Rate and to Whom?

Meralco likes to say their rate is a media palatable P9.80 per kwh which is their average system rate. We, the captive consumers who are residential and commercial users and who comprise more than 60% of their energy sales and probably 75% of their revenue, pay P12.30 per kwh.

The reason for the lower average is because they have designed their revenue mix by reducing the rate to their industrial customers and a significant amount of “lifeline” customers. We the captive customers in what we can call the “middle class” of customers are the ones being made to carry the big burden of overprices. For our purposes, we are seeking a reduction of P3 per kwh (or 24%) from the P12.30 per kwh rate to the captive customers, majority of Meralco’s revenue source.

Shocked at the big amount? Yes, our power cost have not been optimized by that much due to pass on charge unconcern by the utility itself, by regulatory tolerance, market structure defects, and government’s own contribution to the rising costs.

The Reduction in Perspective

At the outset let us make clear that these reductions are not intended to make Meralco unviable. They are entitled to have a fair return on their investment. That return however just has to be consistent with the monopoly protection that came with their public service utility franchise and the regulated nature of a distribution utility.

Of the P3.00 per kwh reduction MSK is seeking only about P0.40 per kwh or 13% will potentially be a reduction in Meralco’s excessive income from PBR. The rest of P2.60 per kwh will be from “pass-on” charges like generation, transmission, systems loss, VAT, and universal charges on which Meralco likes to say they are not making money and only acting as the collector. These reductions in pass-on charges are technically revenue neutral to Meralco and its controlling stockholder, Metro Pacific, and hence they should have no objections. This is Meralco’s best opportunity to prove that they are faithful to their obligation to provide power in the least cost manner and true to their long media claim that they don’t make money on the generation charges.

Areas for Feasible Reduction

What MSK did was to analyze every cost item and identified the FAT resulting from the governing regulatory and systemic rules and practices. Our 10 recommendations are line by line on the cost components of your monthly Meralco electric bill.

No. 1 Generation Charge.

Meralco’s average generation charge that it has been passing on to the consumers is about P5.60 per kwh. We believe this can be reduced to P4.00 per kwh. These are the bases of the estimate.

- Meralco has been buying power from coal power plants at rates ranging from 3.37 per kwh to 4.34 from truly independent power generators. It is 4.43 to 4.66 from its negotiated source, Quezon Power. It is clear therefore that market prices for base load supply can be achieved at lower than P4.00 per kwh. Hence, if Meralco opens its market to competitive bidding, these generation market prices can be achieved.

Metro Pacific and Meralco PowerGen who apparently own 51% of the 400mw expansion of the Mauban Coal facility in joint venture with current owner of Quezon Power, announced in the media that their rate is P4.35 per kwh. For a 25 year contract base load power supply contract, we believe truly independent generators can bid up to 15% lower. And who knows what devils are in the details of the negotiated power supply contract? Consumers need to be provided a safeguard of competitive rates by subjecting this to competitive bidding.

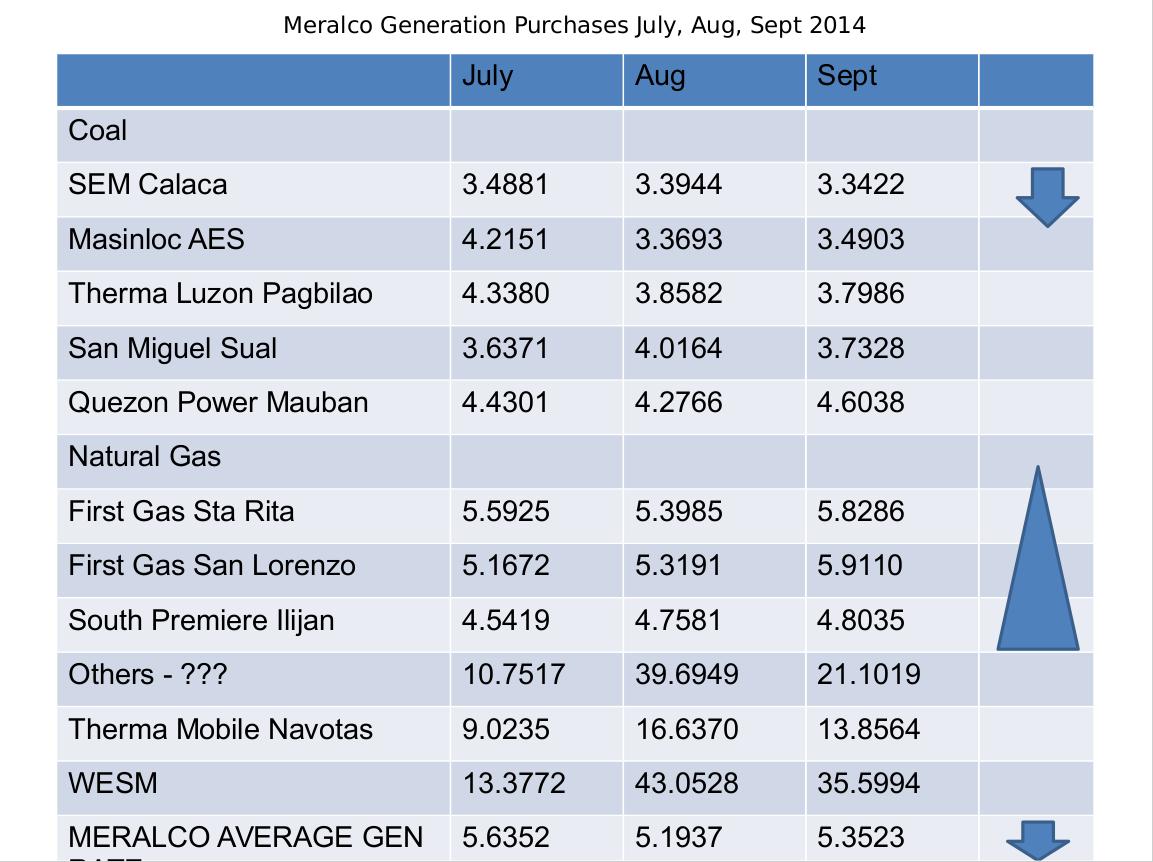

Below is a chart of Meralco’s generation sourcing mix. These are based on Meralco’s own data for the three months July, August, and September 2014.

2. From these Meralco data, we can see the contrasts that point to areas for improvements to reduce power costs:

a. The rates paid to sister power generators are higher by as much as 20% than those negotiated with unrelated truly independent power generators. See First Gas companies compared with the SPPC for the Ilijan plant.

At the DOE task force meetings, Meralco tried to say that First Gas is Not a sister company of Meralco. Our point is those 25 year contracts were negotiated when Meralco was still majority owned by the Lopez group who owned First Gas. The consumers are still suffering from these sweetheart prices 1o years later. Now Meralco PowerGen announced 3,000mw of power projects which corners most of the lucrative contracts of Meralco at rates that they self-deal with themselves.

b. The rates of the Sister Power Producers (SPP’s) tend to increase significantly from time to time due to guaranteed capacity payments when they go on maintenance downtime. These projects have been operating past the original term of their project financings so guarantee of capacity payments even when they are not operating are no longer justified. Instead they can be guaranteed a level of energy purchases but they get paid only when they deliver.

c. Notable by their absences in these Meralco power supply list are the 2,000mw of hydro power in Luzon. Meralco’s energy mix can be improved to include a level of predictable hydro energy and purchases from cheaper sources than the higher ones. From the Meralco prices, one can observe that the more expensive suppliers get the bulk of Meralco’s supply. If Meralco were buying power on “arms-length” basis with true commitment to least cost power, one would think they would be buying more from the cheaper sources.

The 2,000mw of hydro power is apparently being sold by the new private owners through the WESM at market settling prices reaching P33 per kwh as opposed to a contracted P3.50 per kwh. Let us remember that the “fuel” for these hydro power is rain water from the country’s mountain ranges that technically is owned by the public and public domain. Why sell the water energy at P33 per kwh to the people who supposedly own the water?

The new hydro power owners claim that they never know when water will be made available by the National Irrigation Administration for power generation and hence they cannot enter into power supply contracts. That is bunk. There are sure levels of water and energy that can be available in the course of the year for power generation otherwise these private investors would not buy these hydro facilities. The CBK complex is pump hydro and not used for irrigation. Why is this not contracted directly to Meralco?

d. WESM prices continue to wreak havoc on the consumers and urgently needs a change in rules to provide safeguards to consumers. The current “Market Settling Prices” which is the highest price bid and dispatched for the trading period needs to be dropped and paid as bid should be adopted. This will also reduce market manipulation.

If these reforms are undertaken on the generation side and implemented in an honest to goodness manner (meaning no bid rigging and collusion) Meralco will have an achievable chance to reduce its average generation charge to P4 per kwh.

Why should they be allowed to monopolize power supply and self-deal and negotiate the prices and terms at prices ranging from P4 to 6 per kwh. This is so anti-consumer and anti-people and anti-country.

- Applicable Law

There is no need to amend the Epira law to undertake this reform. Section 45 (a) and (b) of the Epira Law of 2001, while allowing contracting of up to 50% of the demand of a DU with an affiliated generator, it is silent on negotiation or bidding. The DOE and ERC therefore has latitude to require open competitive bidding under the current law.

Interestingly, both the ERC and DOE claim that they are working on regulations to mandate competitive bidding for bilateral power supply contracts. The DOE’s DASAP is a recent proposal and lets hope they will do it with urgency. The ERC claims they have one draft proposal since 2007! ERC also presented it to the Phil Chamber of Commer power committee months ago. Why do these urgent safeguards for consumers ever taking so long through the bureaucratic grind? Sometimes you wonder if they are just going through the motion so they can politically say when asked that they have a regulation already in process. In the meantime, 25 year power supply contracts are already being self-negotiated. Ano pang gagawin sa damo…..kung?

Summary:

- Bilateral power supply contracts should be subjected to open competitive bidding. This will also open up the power generation sector to more independent investors with more competitive rates, technologies, and more energy efficient operating systems. This is doable without amending the Epira Law. DOE and ERC just need to step up and do something good for the consumers.

- Meralco should restructure its take or pay agreement with First Gas and QPL so that they are only paid when they provide a service and deliver energy. Not when they are down for maintenance which Meralco should be monitoring diligently and accurately. These SPP’s have operated longer than their original loans so the guaranteed take or pay, operating or not, can be dispensed with to safeguard the consumers from undue rates. First Gas San Lorenzo was paid 9.99 in December 2013 due to these guaranteed capacity payments, operating or not.

- WESM rules must be changed to drop the current “marketing settling price” system that is so anti-consumer. Perhaps they should adopt a reserve market to provide for a more cost effective and predictable availability of reserve power.

- Meralco should improve its energy mix by buying more from cheaper sources and by including hydro power in their contracted power supply.

Generation is only a pass on charge and as Meralco likes to point out they don’t make money on it and only act as collectors. This reform is therefore revenue neutral to them. They must support these reforms in keeping with their responsibility as the franchised public service distribution utility to provide power “in the least cost manner”.

How about it Meralco?